Top consumer trends of 2023

How can you prepare your brand for the rocky year ahead? Using Attest data from 1,000 UK consumers, we’ve identified the top 18 trends to know.

Sentiment trends

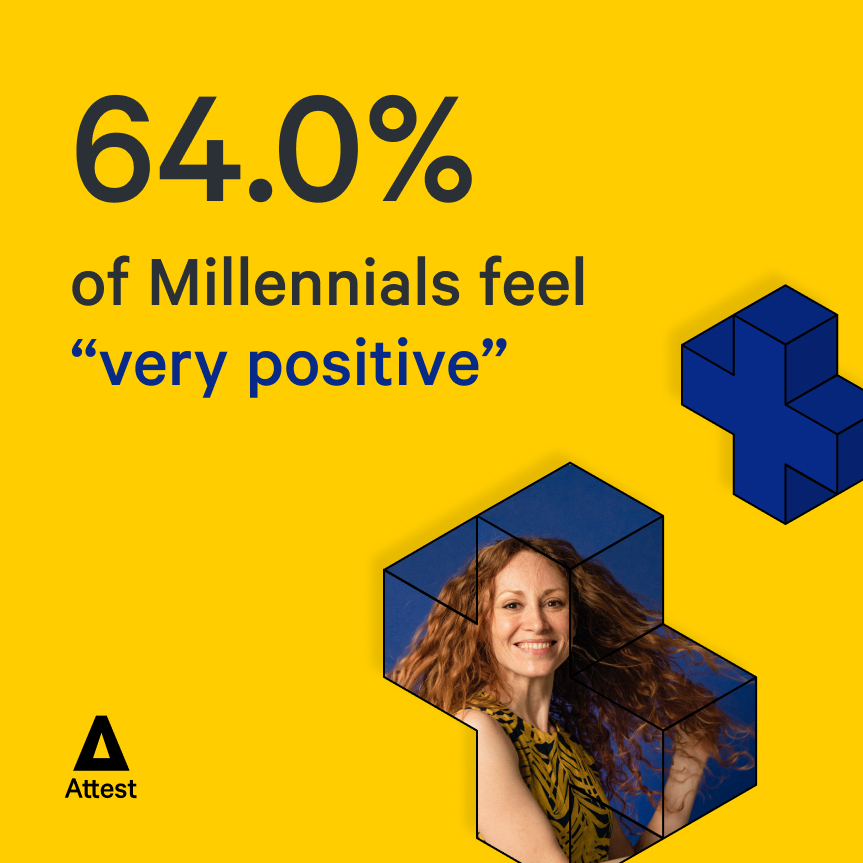

Trend 1: Young people feel positive!

Gen Z are more likely than other demographics to say they’re feeling positive right now: 64.0% in comparison to 45.0% of Millennials and 36.5% of Gen X. And they’re twice as likely as Boomers to describe themselves as feeling “very positive” (14.0% versus 7.1%).

Overall, though, inflation has taken its toll on the positivity of the nation. Positive sentiment has declined by 11.4 points from a year ago, now standing at 41.1%.

Top tip: Adjust your messaging – older and younger consumers have notably different outlooks.

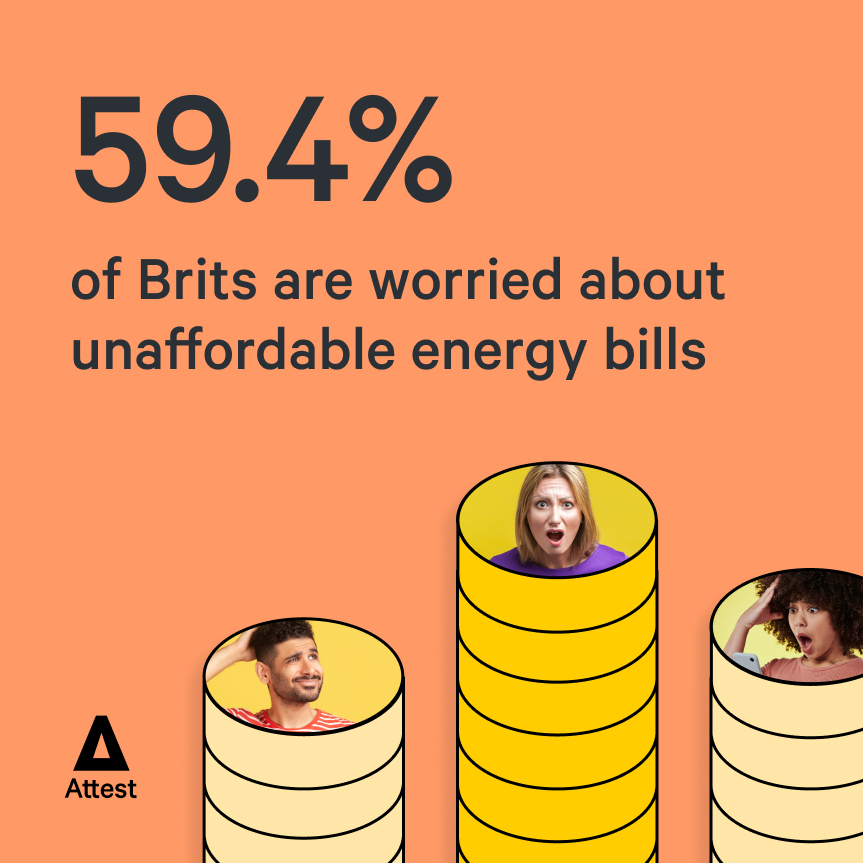

Trend 2: Energy bills are a big issue

More than half of consumers are worried about being able to afford their energy bills, making it the issue Brits are most concerned about heading into 2023.

But other fears vary across demographics; Gen Z are 2x as likely to be fretting about petrol prices, while Boomers express more worry about the war in Ukraine.

Top tip: Identify your target consumers’ worries and find ways to support them, for example, through partnerships with other brands.

Want to drill down further?

Send a survey to target consumers.

Get started for free

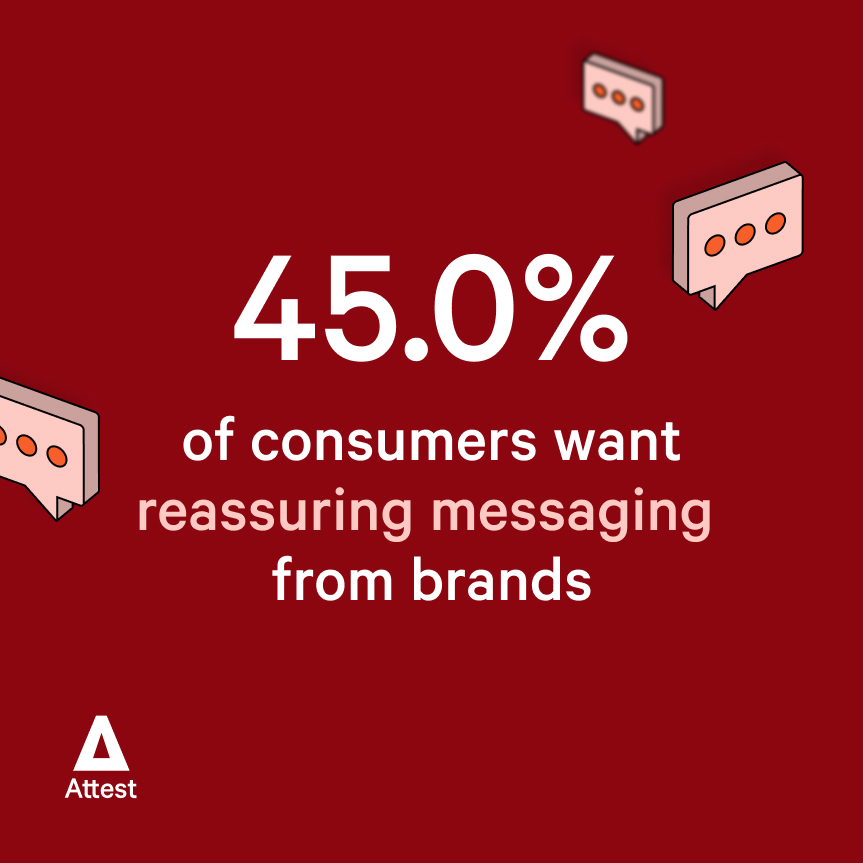

Trend 3: Brits want to be reassured

Consumers want to be told everything’s going to be alright; we see an 11.4 point uplift in the number of consumers who want to hear reassuring messaging from brands, to 45.0%.

Overall, humorous messaging is slightly more popular (at 48.8%) but this is very much driven by consumers aged 40+. Younger consumers, on the other hand, show a preference for motivational messaging.

Top tip: Reassuring messaging is popular across demographics – aim to make your brand feel like a safe and caring place.

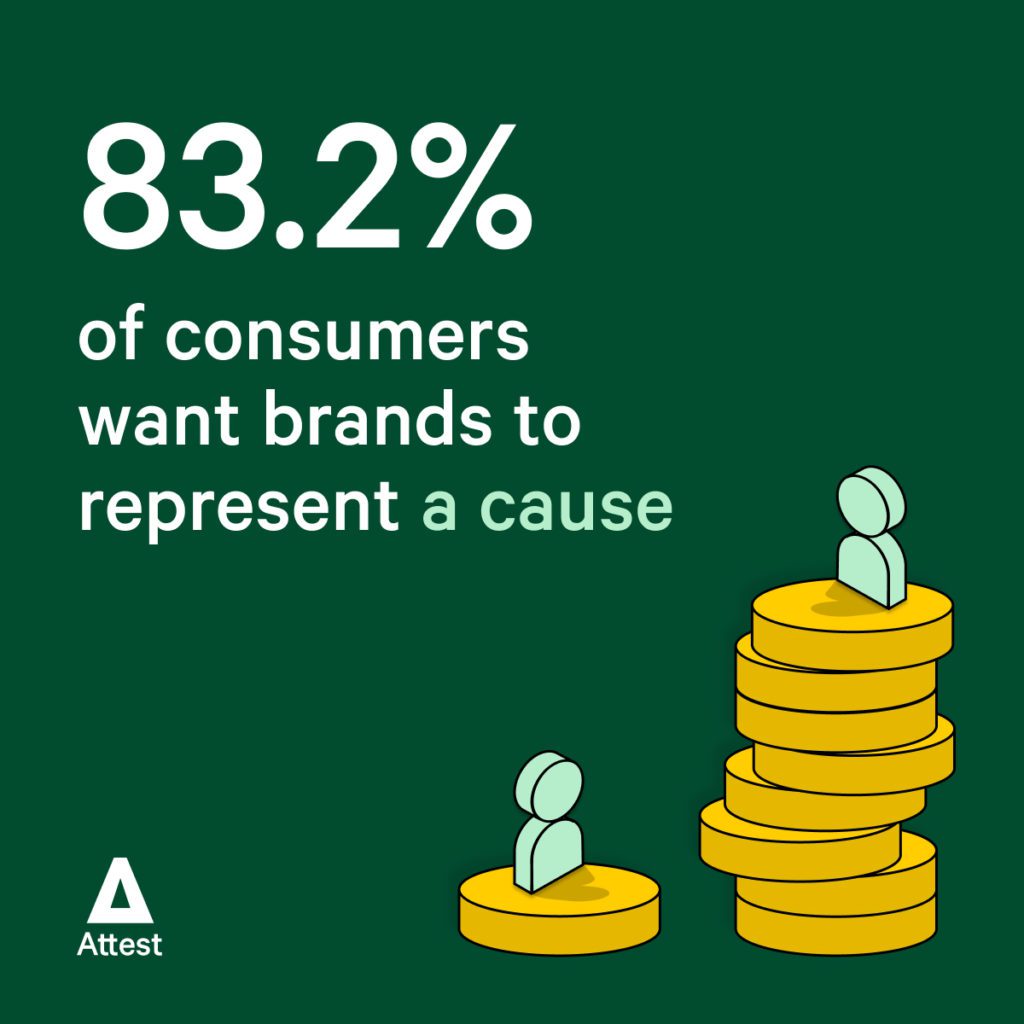

Trend 4: Brands must “be political”

There’s a growing desire for brands to take a stand on political and social issues. We see this in the 11.4 point increase in people wanting brands to act on poverty and inequality.

Overall, 45% of consumers want brands to address poverty and inequality. This is followed by climate change (41.4%). Gen Z, meanwhile, are significantly more likely than other demographics to want action on racism (47.2%).

Top tip: Playing it safe may no longer be an option for brands who really want to represent their consumers.

Marketing trends

Trend 5: Under 40s ❤️ brand comms

Gen Z and Millennials are significantly more likely than older demographics to welcome frequent marketing emails from brands they’re interested in: over 30% welcome contact more than once a week.

But email remains a valuable channel for brands to reach all age groups, with ‘once a week’ being the preferred cadence for mailings. The percentage of consumers who don’t want to receive marketing emails is just 10.8% (down 3.2 points on 2021).

Top tip: Ramp up your email marketing to stay front of mind, but make it worth your customers’ while with discounts and exclusive offers.

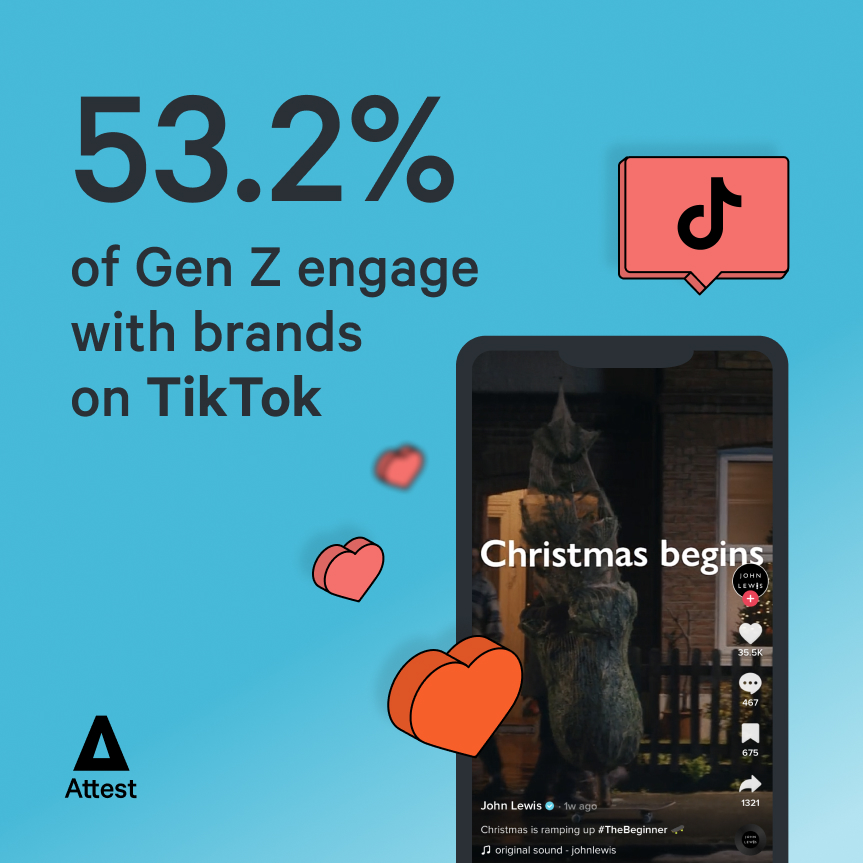

Trend 6: TikTok taking off for brands

The number of consumers who engage with brands on TikTok has increased by 7.4 points since last year, to 27.1%. Gen Z are driving the growth: 53.2% interact with brands on TikTok.

Instagram also sees a 11.5 point hike to 50.8%, putting it ahead of Facebook for brand interaction. Overall, engagement with brands on social media has increased by 7.8 points to 83.5%.

Top tip: TokTok content needs to have an authentic, homemade quality, so be prepared to bend your brand guidelines.

What’s the outlook for your brand?

Speak to your customers today

Send a free survey

Trend 7: VR marketing is an opportunity

Ownership of virtual reality headsets is growing; more than a quarter of UK households have one. Consumers aged 40 and under are the biggest adopters of VR, 32.2% have a headset (including 5.2% who own more than one).

A further 25.3% of Brits who don’t have a VR headset state they plan to get one. Boomers are least likely to adopt VR technology, with 69.2% saying they have no plans to use it.

Top tip: Advertising opportunities in virtual worlds include billboards that brands can use without knowledge of the metaverse.

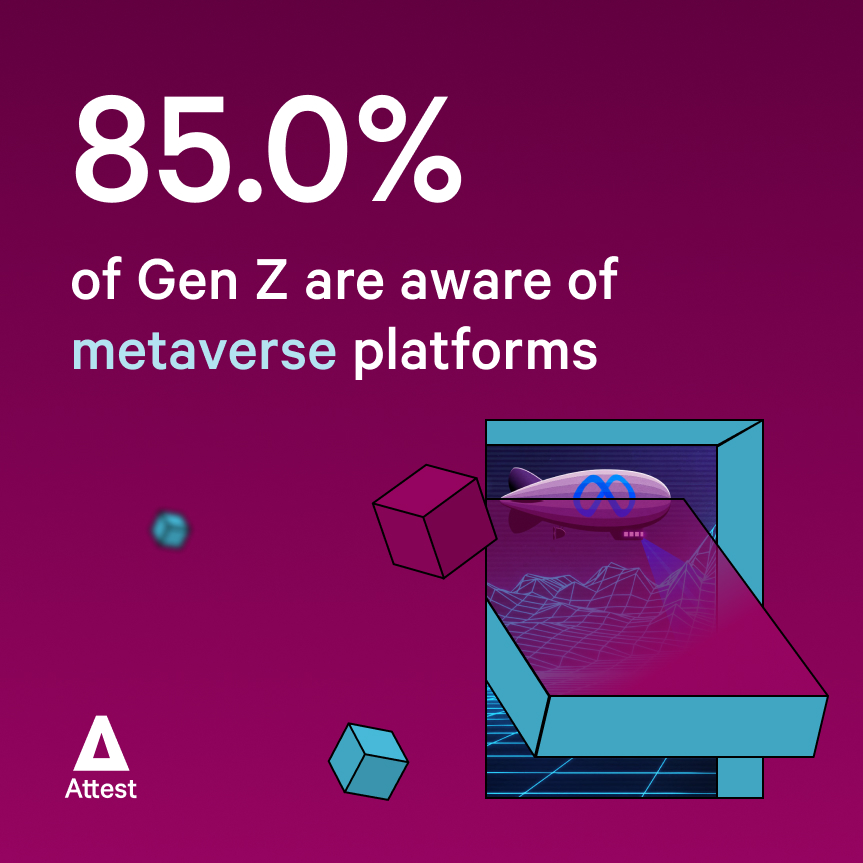

Trend 8: Gen Z populate metaverse

Gen Z have the highest awareness of metaverse platforms, with 85.0% familiar with at least one. Roblox – a virtual world for kids – has the strongest awareness: 67.6% of Gen Z know it.

However, only 11.7% are familiar with Meta Horizon Worlds (Mark Zuckerberg’s offering), suggesting the platform is some way off becoming mainstream.

Top tip: Brands can create virtual products in Roblox, using it as a shop window to attract young consumers (and their parents).

Shopping & spending trends

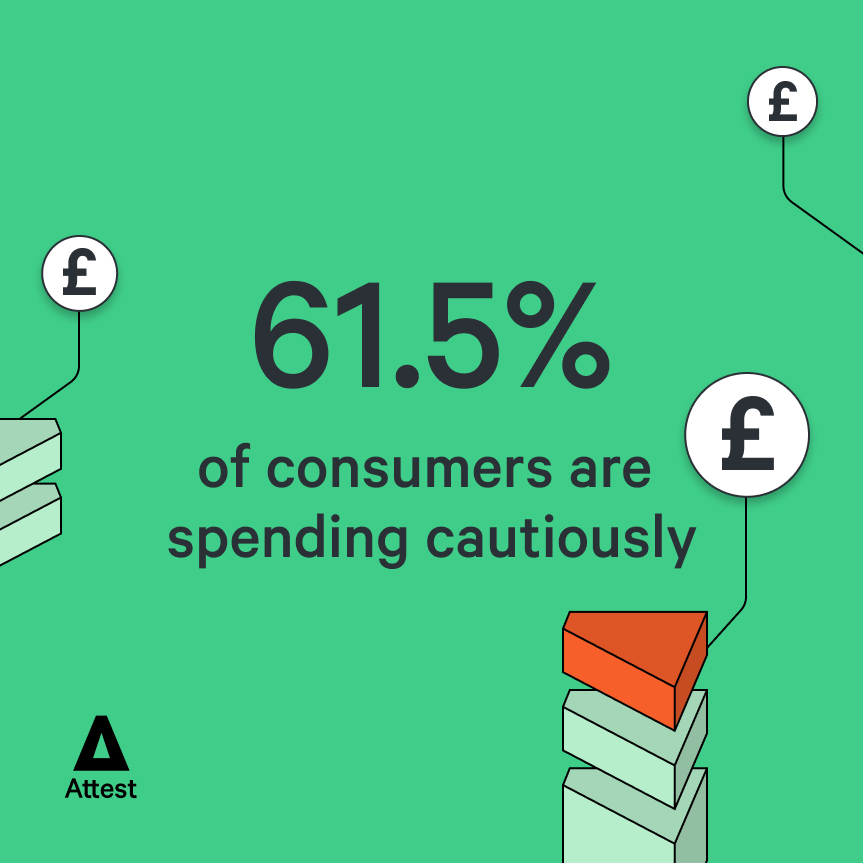

Trend 9: Consumers spend cautiously

It’s no surprise that inflation is having an impact on consumer spending, but our data highlights the change on last year: we see a 10.2 point increase in “fairly cautious” spending and a 9.1 point increase in “very cautious” spending.

Older consumers are twice as likely to be keeping a tight hold of the purse strings: 26.9% of Boomers are spending “very cautiously” versus 12.8% of Gen Z.

Top tip: Focus on value-driven messaging, especially for shoppers aged 40 and older.

Trend 10: Older shoppers favour stores

The pandemic increased adoption of online shopping among older consumers, but Boomers are returning to the high street. Over 40% of Boomers say they now “mostly or always” shop in-store.

Younger shoppers, on the other hand, still favour online: 47.2% of Gen Z and 49.7% of Millennials “mostly or always” shop online.

Top tip: A third of Brits split their purchases between online and in-store, meaning multi-channel distribution is the safest bet.

Attest gives us the confidence to run market research that we know will reveal or compound actionable knowledge about our market.

Siamac Rezaiezadeh, Director of Product Marketing, GoCardless

Trend 11: Amazon loses market share

We can’t say if it’s as a result of campaigns to boycott Amazon or simply down to reduced consumer spending, but our data shows a net -5.9% of Brits plan to shop less on the marketplace in 2023.

The biggest cutbacks will be made by Gen X, a net -13.1% of whom say they’ll reduce spending on Amazon. Meanwhile, Gen Z have plans to switch to superstores like Tesco and Asda: a net +15.2% will shop in them more, bucking an otherwise downward trend.

Top tip: Promote the benefits of shopping directly with your brand for shoppers who want a more ethical alternative to Amazon.

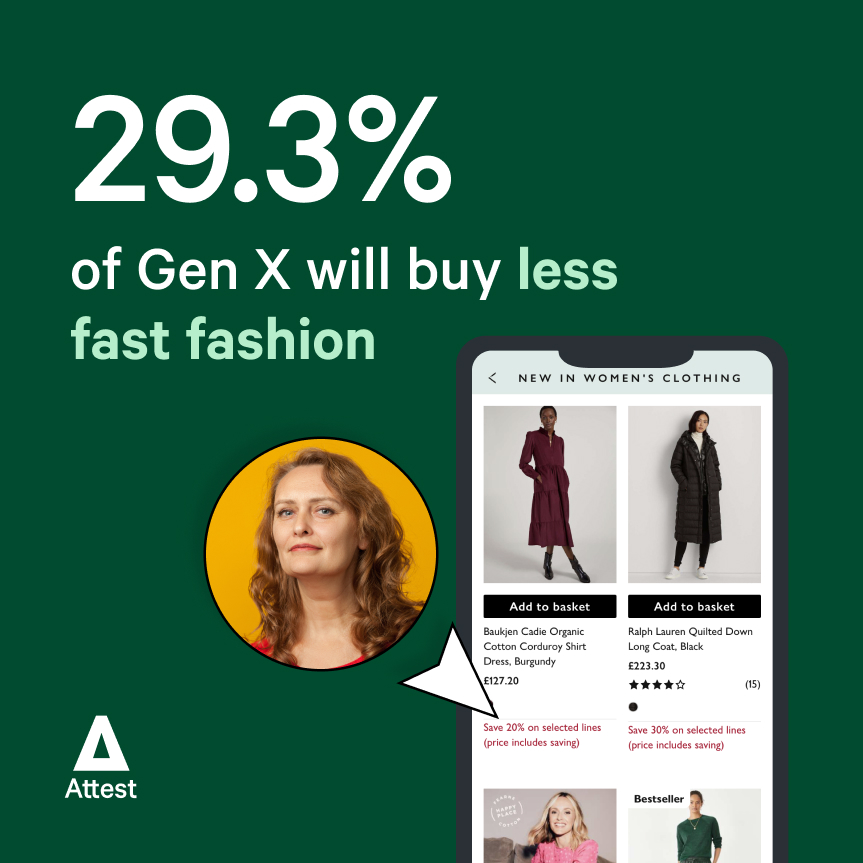

Trend 12: Fast fashion faces a reckoning

The environmental impact of fast fashion has been in the spotlight lately and it seems to have had an impact. A net -23.5% of consumers say they will buy fewer fast fashion items in 2023.

Gen X consumers are especially likely to make this commitment, with a net -29.3% planning to buy less. But fast fashion’s biggest consumers (Gen Z) will also cut back: -21.6% net.

Top tip: Join clothing brands like PrettyLittleThing, Zara and Shein by introducing a resale platform to help reduce waste.

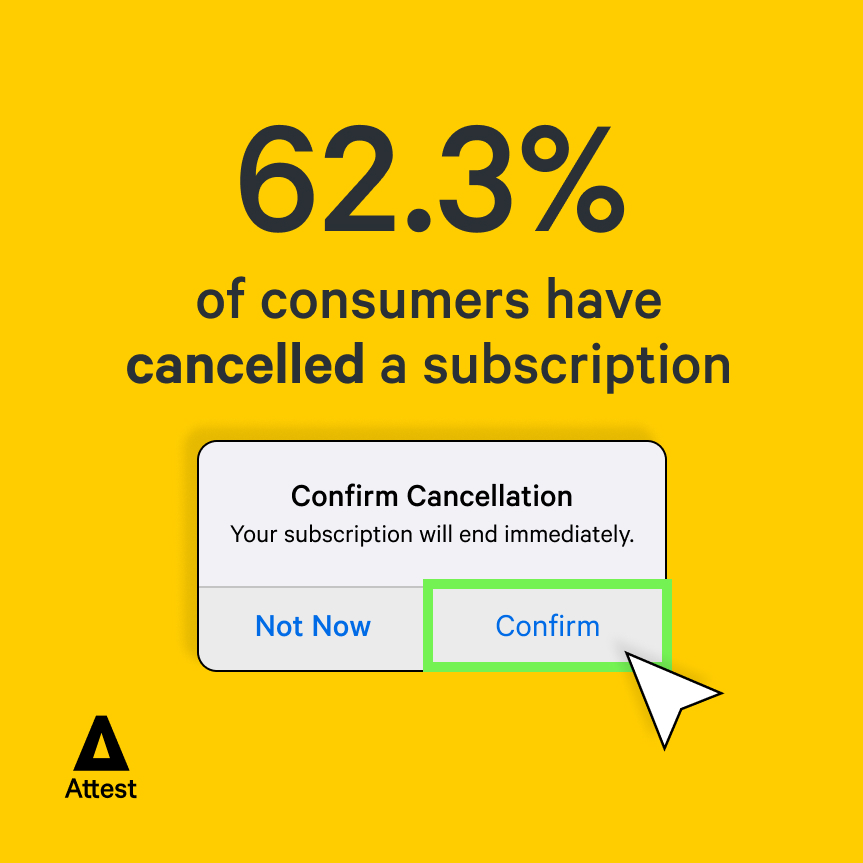

Trend 13: Streaming services chopped

Subscriptions are a casualty of the rising cost of living, with 62.3% of consumers cancelling one. More than 22% have axed a TV streaming service to cut costs and 14.8% have cancelled a music streaming service.

Younger consumers are more likely to cancel: 20.9% of Millennials have cancelled a meal kit subscription, while 24.1% of Gen Z have cancelled a physical gym subscription and 20.9% have stopped their Amazon Prime subscription.

Top tip: Introduce the ability to pause subscriptions rather than lose customers altogether.

Lifestyle trends

Trend 14: Shopping frequency is up

Despite having less money to spend, consumers aren’t going to the shops any less frequently; we see a 6.2 point increase in people shopping “daily” and “weekly”, to 65.5% (a trend largely driven by shoppers over 40).

Doing sport at least once a week has also grown in popularity by 6.1 points (42.5%), with Gen Z the most active. Meanwhile, the percentage of people going out for a meal less frequently than monthly has increased by 7.5 points to (32.1%).

Top tip: Refresh retail offers and POS displays regularly to keep high frequency shoppers engaged.

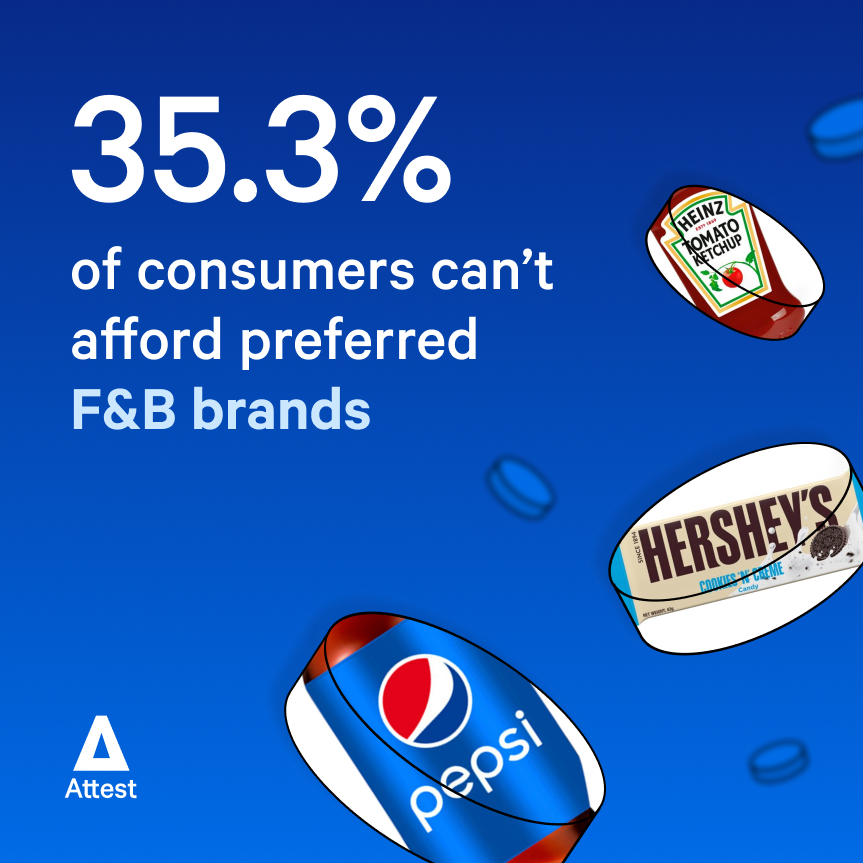

Trend 15: Diets changing (for the worse)

More than 20% of consumers say the rising cost of food is having a “big” impact on their diets, while a further 39.8% say it’s having a “medium” impact.

Nearly 36% are experiencing difficulty affording fresh quality foods like meat, fruit and vegetables (40.9%), while 35.3% can no longer afford their preferred brands and 37.8% struggle to eat out.

Top tip: Reduce pack sizes to bring down the retail price and keep your customers.

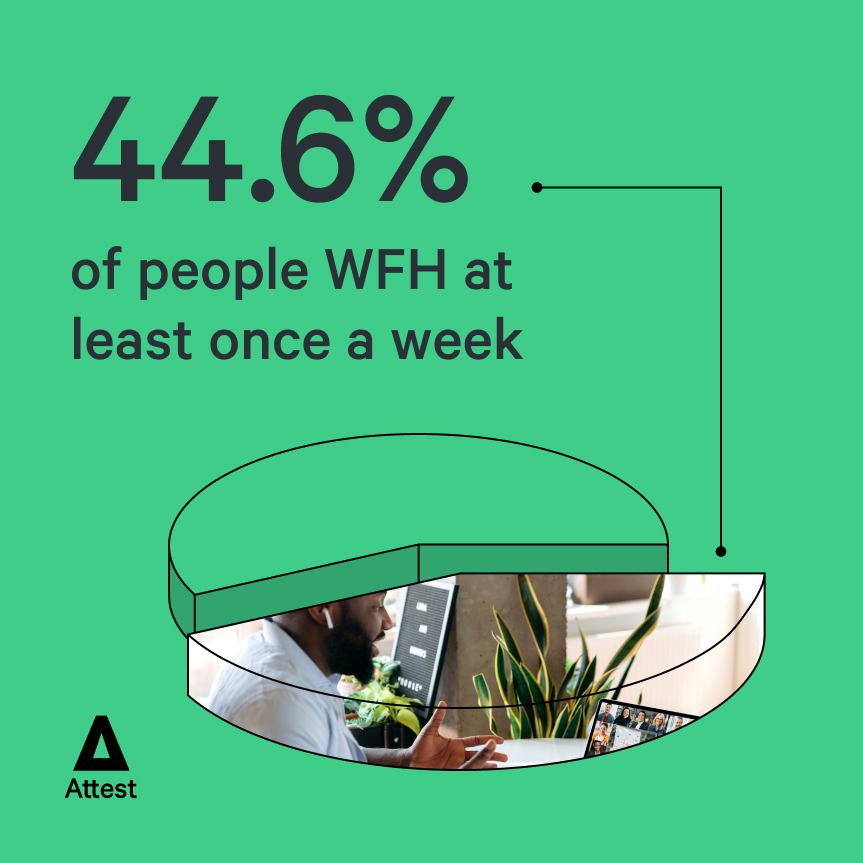

Trend 16: WFH here to stay

Elon Musk might be trying to put a stop to it at Twitter, but our data evidences only a small decline in the WFH movement since last year, with a +4 point increase in the number of workers who never work from home (28.8%)

Nearly a third of people split work between home and the office, while 12.0% work from home five days a week.

Top tip: Reconsider advertising that targets commuters, which might not be as effective due to reduced traffic.

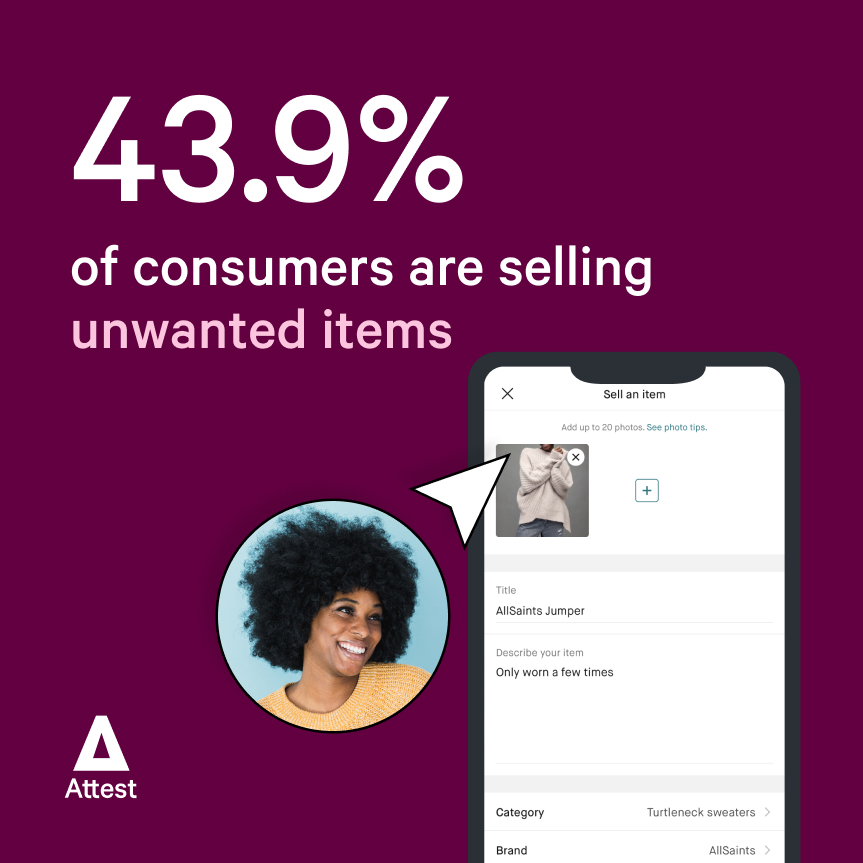

Trend 17: Second hand losing its stigma

Second hand shopping will be a big pastime in 2023, with 34.8% of consumers saying they’ll be hunting for charity shop bargains to combat the rising costs of inflation.

In turn, nearly 44% of consumers will be selling their unwanted goods – especially Millennials – meaning the pre-loved market will be booming.

Top tip: Tap into the thrifty mindset with ideas to help consumers reuse and recycle goods.

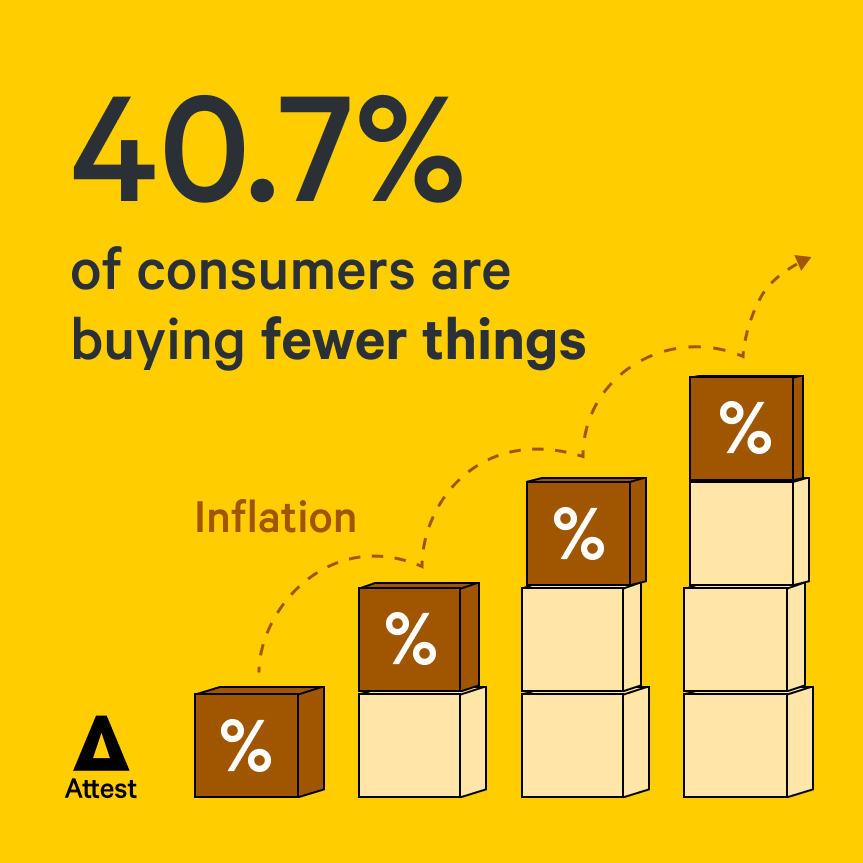

Trend 18: Rampant consumerism is out

Frugality is cool; 40.7% of consumers say they are buying fewer things and consuming less – that’s an 8.5 point increase on last year.

Another environmental trend sees Brits cutting down on their car usage, with a 6.7 point increase in the number of people ditching their cars, to 32.5%.

Top tip: While price is the primary motivator for 2023, quality should not be overlooked as consumers look to buy fewer things and keep them for longer.

What opportunities do these trends represent for your brand?

Get more data

Get a direct line to

inflation-squeezed consumers

Quick and easy to run surveys

Get going in minutes with our intuitive platform and get results quickly, our average survey closes in 1 day 19 hours.

High data quality

We use automated and human checks on your data, you can be sure you’re making the right business decisions.

Research guidance

You’ll be supported by a dedicated industry professional every step of the way to help you get the most from your research.

Find your target audience

Our audience lets you access 150+ million people across 59 countries, and use filters and quotas to make it as targeted as you need.