Over the past few years, Gen Z has consistently been framed as the generation “drinking less.” But what’s more interesting in 2026 is how that behavior is evolving.

This isn’t just a story of decline – it’s a story of redefinition.

Gen Z is reshaping when, where, and why alcohol is consumed. Drinking is becoming less frequent, more intentional, and increasingly optional within social settings.

To understand what’s driving these changes, we surveyed 800 US Gen Z consumers aged 21–27 using Attest’s platform and compared the results with data from the previous year.

What emerges is a clearer picture of a generation becoming more cautious, selective, and context-driven in their relationship with alcohol.

TL;DR: Gen Z alcohol trends 2026

Definition:

Gen Z alcohol trends reflect how 21–27-year-olds are shifting toward moderation, home-based consumption, and more flexible drinking habits shaped by health, values, and convenience.

Key insights:

- Moderation is increasing – 24% don’t drink at all, and over half drink rarely or not at all

- Home drinking has surged – rising from 42% to 64% year-on-year

- Non-alcoholic options are growing – with more consumers moving from curiosity to regular use

- Convenience formats are booming – ready-to-drink and hard seltzers are seeing rapid growth

- Transparency is expected – around half want ingredient and calorie information

- Brand values carry risk – over half would boycott brands that don’t align with their beliefs

Strategic implication:

Alcohol brands must adapt to a lower-frequency, higher-intention consumer – where relevance depends on flexibility, transparency, and occasion-based positioning.

How Gen Z drinking habits are changing over time

Comparing our 2026 data with the previous wave reveals a clear direction of travel.

The biggest shifts are not in what Gen Z drinks – but in how often, where, and under what conditions they choose to drink at all.

We’re seeing:

- A continued move toward moderation

- A sharp shift toward home-based consumption

- Growing adoption of non-alcoholic alternatives

- Increasing selectivity in both brand and product choices

Taken together, these trends point to a generation that is not rejecting alcohol entirely – but reframing its role in their lives.

What are the latest Gen Z alcohol trends in 2026?

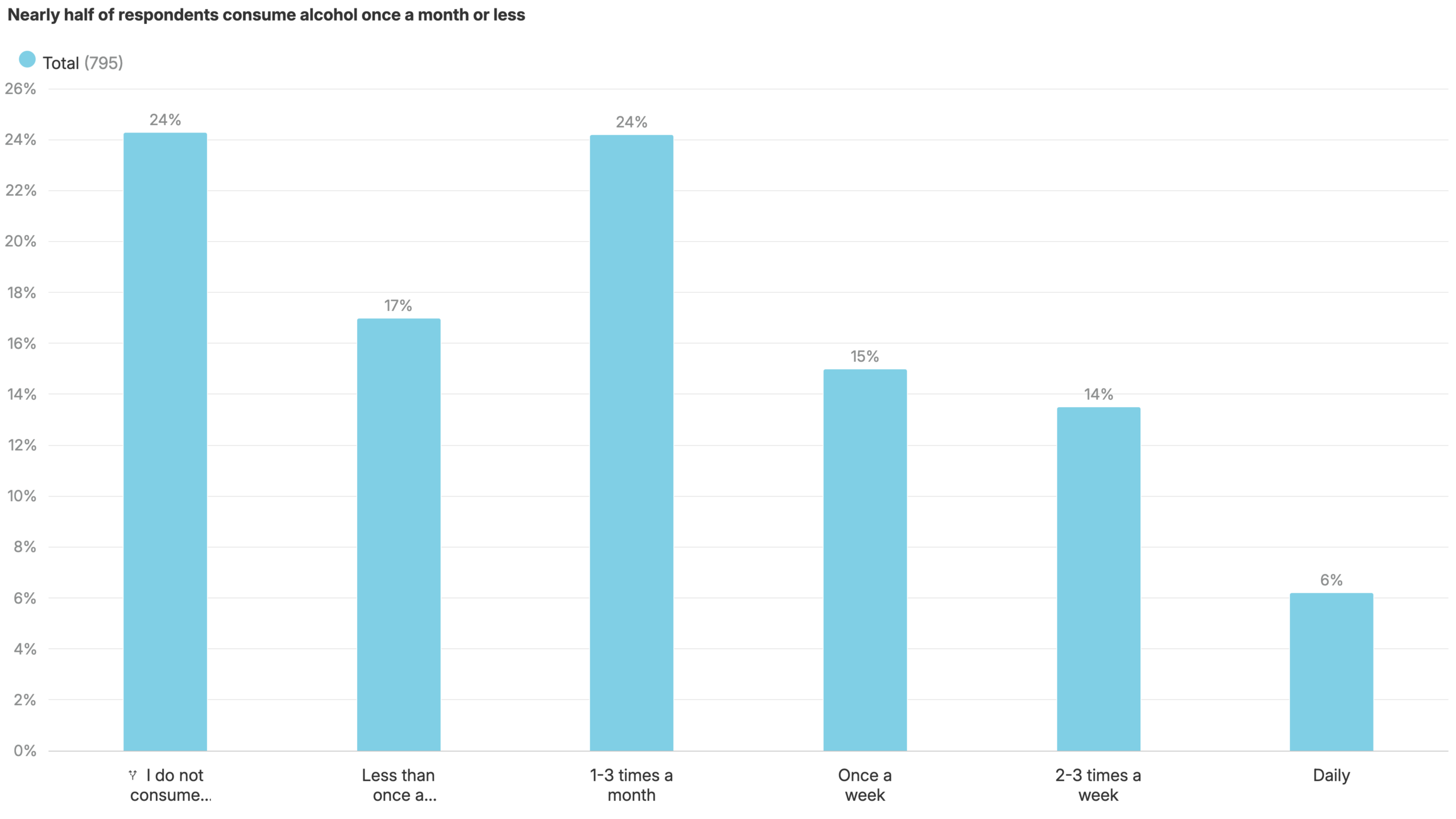

Trend #1: Most Gen Z drink rarely or not at all

Most Gen Z drink alcohol infrequently or not at all, and moderation is increasing year-on-year.

In 2026, 24% of Gen Z report not drinking at all, up from 17% the previous year. At the same time, daily drinking has dropped significantly, from 6% to just 2% .

What’s really happening here:

This is a long-term behavioral shift rather than a temporary trend.

Gen Z is:

- Drinking less frequently

- Avoiding habitual consumption

- Replacing alcohol with alternative ways to socialize

Health plays a major role, particularly around mental wellbeing, but so does a broader cultural shift. Drinking is no longer seen as a default part of social life.

Key takeaway:

Alcohol is becoming an occasional choice rather than a routine behavior for Gen Z.

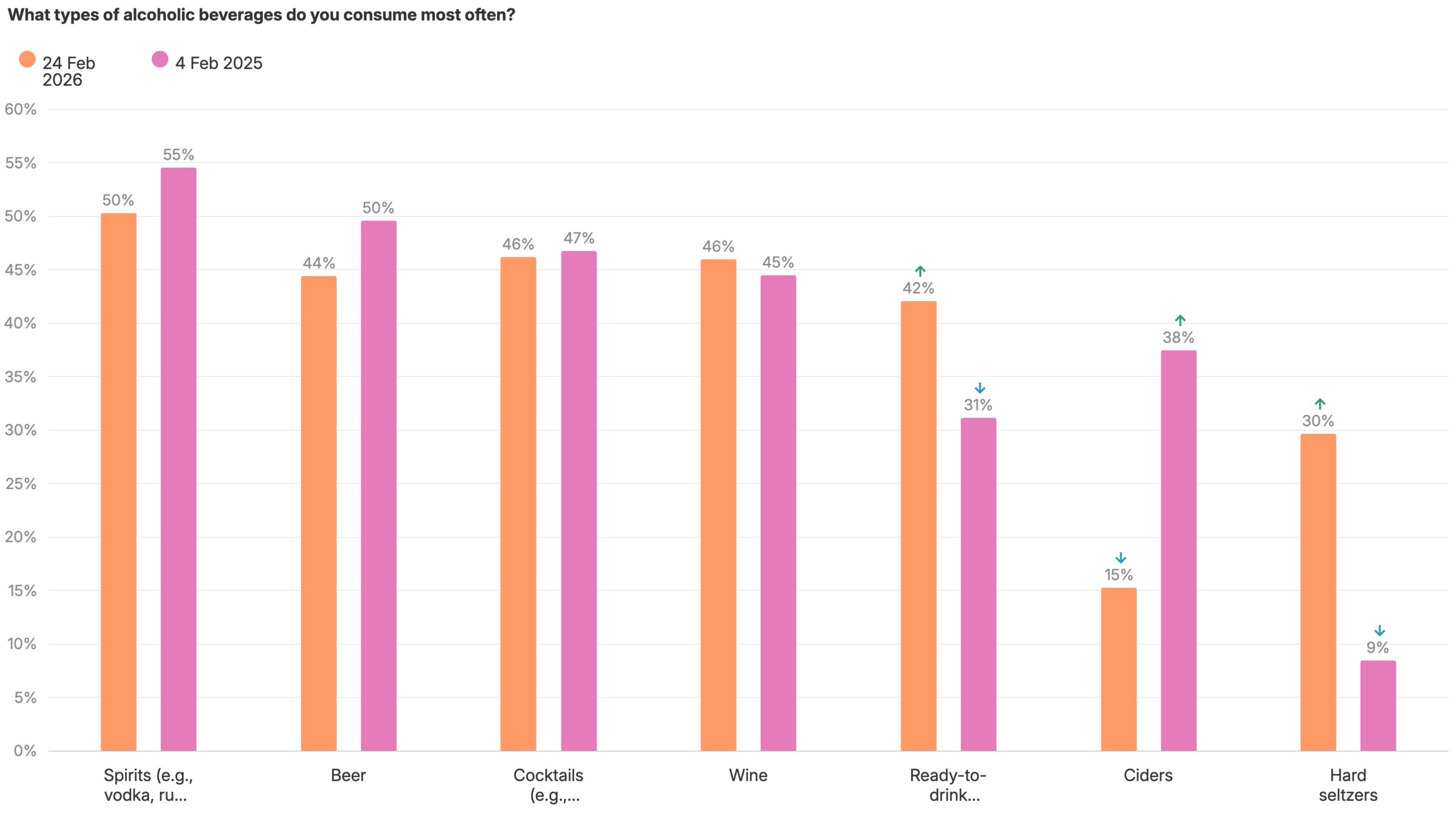

Trend #2: What do Gen Z drink? Convenience-led formats are growing – while some traditional categories decline

Gen Z’s drink preferences are shifting toward convenience-led formats, while some traditional categories are losing relevance.

While core categories like spirits (50%), cocktails (46%), wine (46%), and beer (44%) remain widely consumed, the biggest movement is happening within formats:

- Ready-to-drink beverages have grown significantly (31% → 42%)

- Hard seltzers have more than tripled (9% → 30%)

At the same time, not all categories are benefiting from this shift:

- Cider consumption has dropped sharply (38% → 15%), losing nearly two-thirds of its audience

What’s really happening here:

This isn’t just about taste – it’s about context and convenience.

Growth categories share common traits:

- Easy to consume

- Pre-mixed or low-effort

- Well-suited to at-home or casual settings

By contrast, cider’s decline suggests:

- Less alignment with current drinking occasions

- Weaker positioning in convenience-led formats

- Reduced cultural relevance among younger consumers

In other words, Gen Z isn’t abandoning alcohol categories wholesale – they’re reshaping the formats that fit their lifestyle.

Gender differences still reinforce this shift:

- Men continue to favor beer

- Women over-index on cocktails and ready-to-drink options

Key takeaway:

Category growth is no longer evenly distributed – convenience-led formats are winning, while less adaptable categories are losing share.

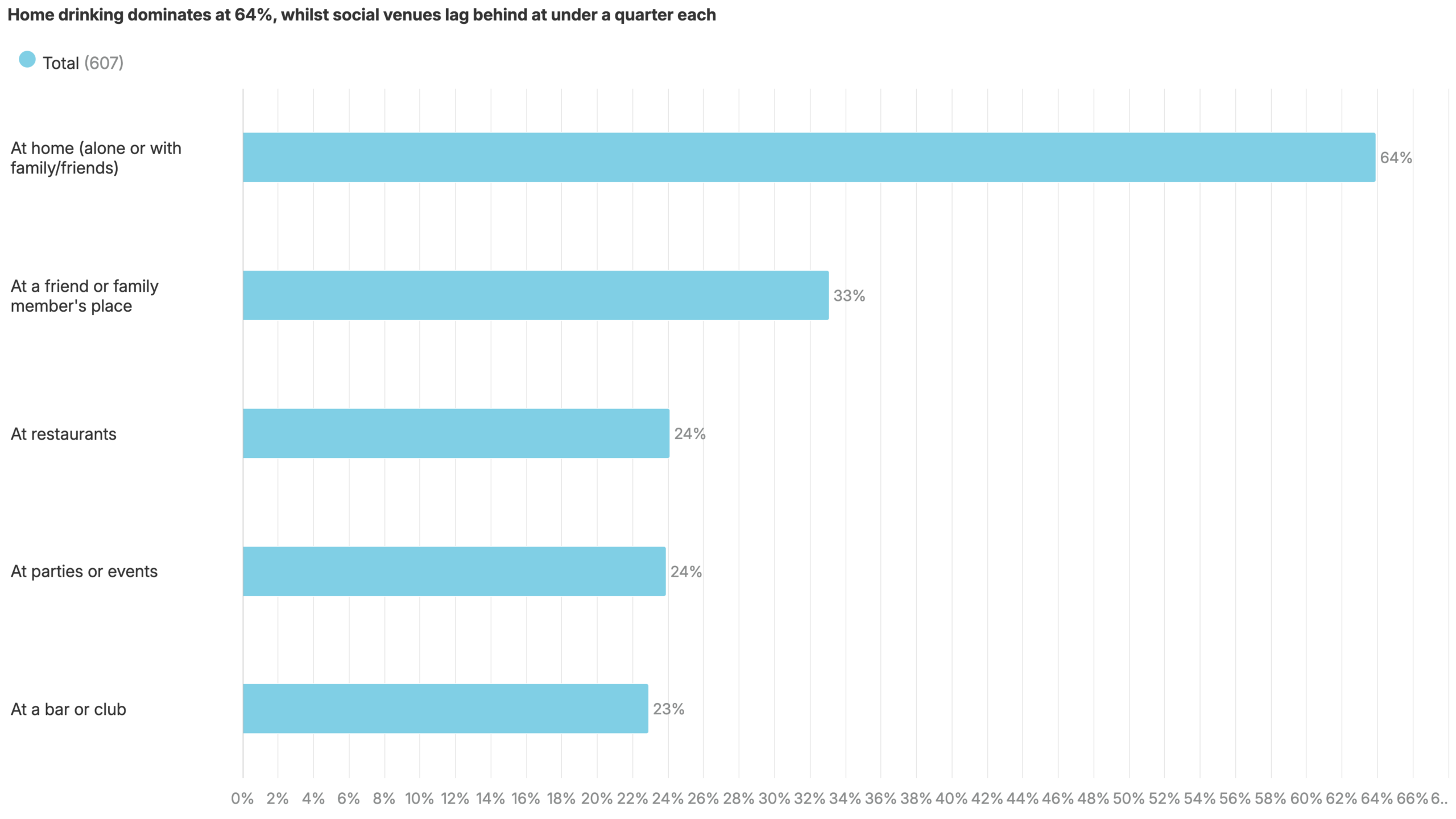

Trend #3: At-home drinking now dominates Gen Z consumption

Gen Z now overwhelmingly drinks at home, with a dramatic year-on-year shift away from bars and clubs.

64% of Gen Z report drinking primarily at home, up from 42% the previous year. Meanwhile, bar and club consumption has dropped from 45% to 23% .

What’s really happening here:

This is one of the most significant changes in the data.

Gen Z is:

- Prioritizing comfort and familiarity

- Reducing spend on nights out

- Reframing social drinking as a smaller-scale activity

This shift also connects directly to other trends:

- The rise of ready-to-drink formats

- Lower overall consumption

- Reduced reliance on nightlife venues

Key takeaway:

Home has replaced bars as the primary setting for Gen Z drinking.

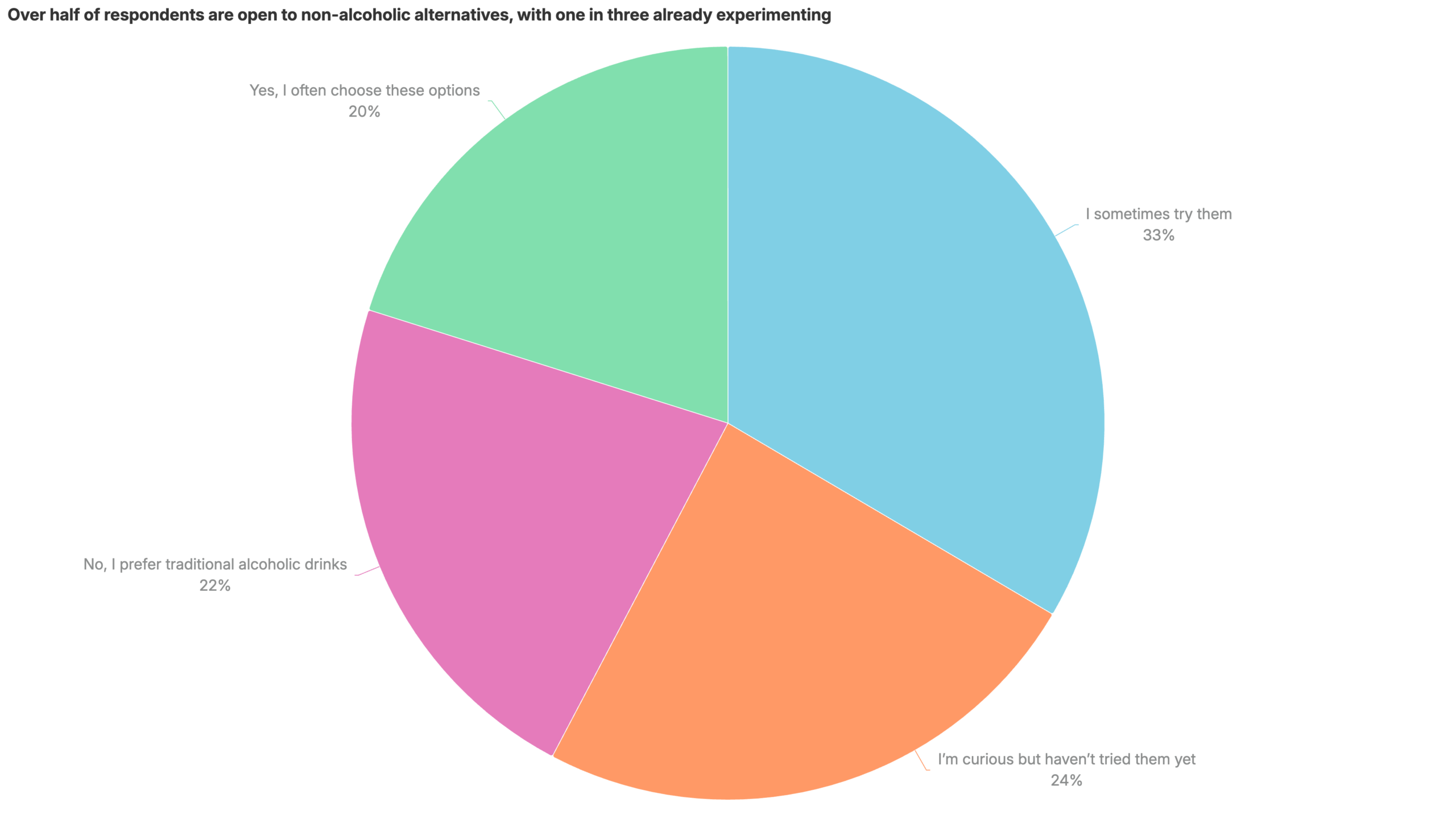

Trend #4: Are non-alcoholic drinks growing? Yes – and usage is deepening

Non-alcoholic and low-alcohol alternatives are moving from curiosity to regular consumption.

Over half of Gen Z are now engaging with these alternatives in some way, with a clear shift toward more frequent use.

Year-on-year changes show:

- “Often choosing” alternatives increased (16% → 20%)

- “Sometimes trying” decreased (44% → 33%)

- Curiosity continues to grow

What’s really happening here:

This reflects a broader move toward flexible consumption.

Gen Z isn’t choosing between drinking and not drinking – they’re:

- Switching between alcoholic and non-alcoholic options

- Matching consumption to occasion

- Maintaining social participation without alcohol

Key takeaway:

Non-alcoholic options are becoming a normal part of drinking occasions, not a niche alternative.

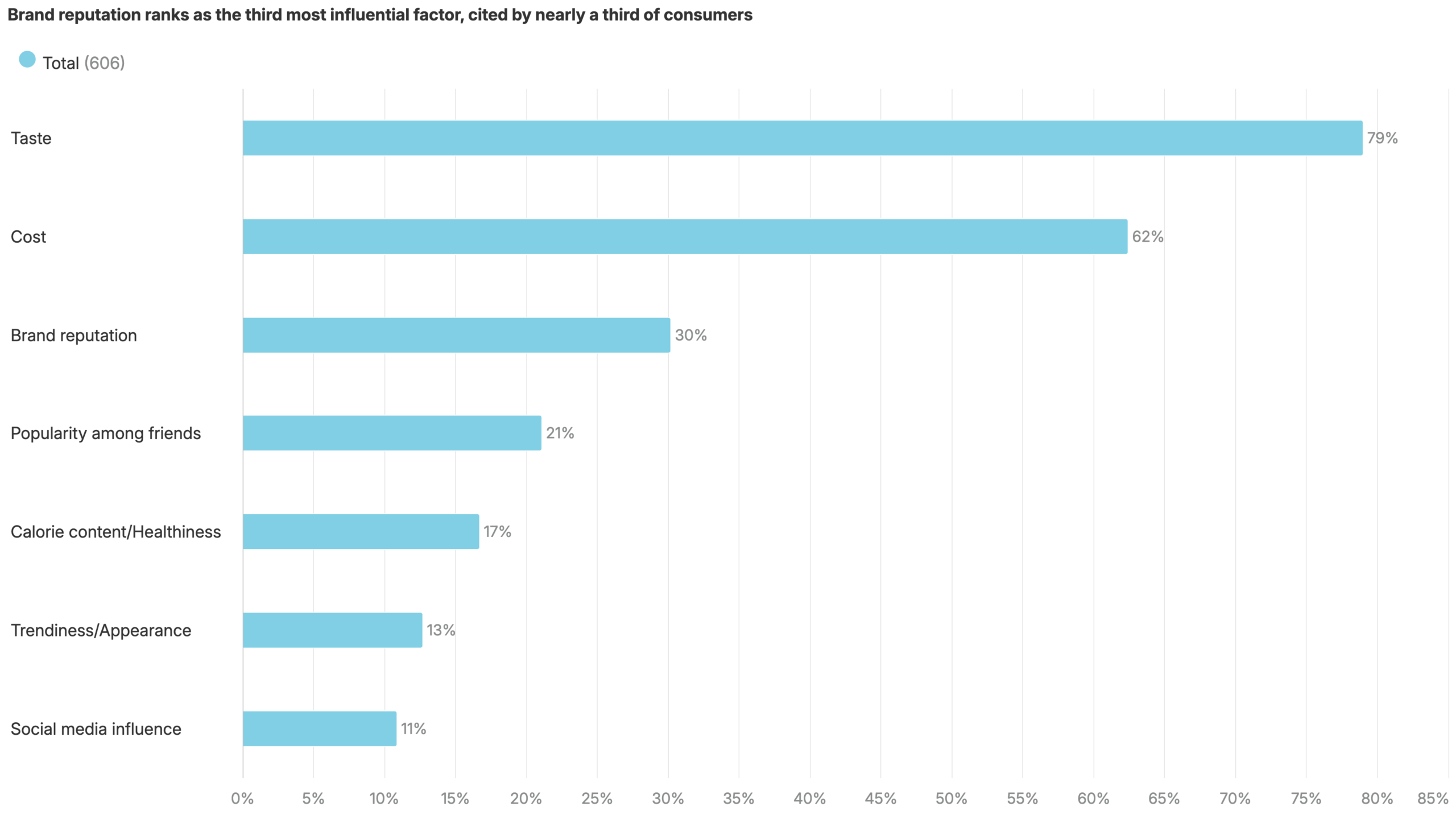

Trend #5: What matters most when Gen Z choose alcohol? Taste leads – but values and reputation are rising

Taste and cost remain the primary drivers of Gen Z alcohol choices, but brand reputation and values are becoming more important over time.

Taste and price continue to dominate decision-making, reinforcing that alcohol remains a functional and experiential purchase first.

But beneath these core drivers, we’re seeing a clear shift in secondary factors:

- 30% now factor in brand reputation, up from 26% in 2025

- The share saying brand values are “very important” has increased from 13% to 18%

- The importance of sustainability and ethical practices has also risen, with 18% stating they’re “very important” up from 12%

What’s really happening here:

Gen Z’s decision-making is becoming more layered.

At a surface level:

- Taste and cost drive the final choice

But underneath:

- Brand reputation is gaining influence

- Values are becoming more meaningful

- Ethical expectations are strengthening

This suggests a shift toward “conditional purchasing”:

- Products must meet baseline expectations (taste, price)

- Then pass additional filters (reputation, values)

Key takeaway:

Taste and price win the decision – but reputation and values increasingly determine which brands make the shortlist.

Trend #6: Will Gen Z boycott alcohol brands? Values matter most when they’re violated

Gen Z may not always choose brands based on values – but they will reject them if those values are misaligned.

While importance of brand values is rising (with “very important” increasing from 13% to 18%), the more telling signal is behavioral:

- 54% say they would likely or very likely boycott a brand that conflicts with their beliefs

- The intensity of this has increased, with “very likely to boycott” rising from 13% to 19% year-on-year

What’s really happening here:

Values act less as a pull factor and more as a filter or veto.

Gen Z:

- Doesn’t always reward brands for aligning with their beliefs

- But will actively penalize brands that don’t

This creates an asymmetric dynamic:

- Limited upside for “good” behavior

- Significant downside risk for misalignment

Importantly, this behavior is consistent across demographics, suggesting it’s a core generational trait, not a niche mindset.

It also connects directly to broader trends:

- Increased awareness of brand actions

- Higher expectations around transparency

- Greater willingness to switch brands

Key takeaway:

Brand values alone won’t necessarily win Gen Z customers – but getting them wrong can quickly lose them.

Additional Gen Z alcohol insights

Does price influence Gen Z alcohol purchases?

Price remains a meaningful factor, even if it’s not always stated as the top priority.

While taste is most commonly cited, ranking data shows price frequently comes second in importance.

Insight:

There’s a gap between stated preference and actual behavior – price still plays a key role in final decisions.

How important is taste to Gen Z drinkers?

Taste is the most cited driver, with 65% prioritizing it.

However, this often overlaps with drink type, suggesting consumers use category as a proxy for taste.

Insight:

Taste matters – but it’s closely tied to format and familiarity.

Where do Gen Z buy alcohol?

Most Gen Z still purchase alcohol through:

- Supermarkets

- Liquor stores

Online purchasing remains limited.

Insight:

Even digitally native consumers rely on physical retail for alcohol purchases.

How Gen Z alcohol behavior is shifting over time

| Trend area | 2025 data | 2026 data | What’s changed |

|---|---|---|---|

| Non-drinkers | 17% | 24% | Significant rise in abstinence, reinforcing the moderation trend |

| Daily drinking | 6% | 2% | Sharp decline in frequent consumption |

| At-home drinking | 42% | 64% | Major shift toward home-based consumption (+22pp) |

| Bar & club drinking | 45% | 23% | Rapid decline in traditional nightlife settings |

| Ready-to-drink beverages | 31% | 42% | Strong growth in convenience-led formats |

| Hard seltzers | 9% | 30% | Fastest-growing category, more than tripling in usage |

| Cider consumption | 38% | 15% | Steep decline in a traditional category |

| Often choosing non-alcoholic options | 16% | 20% | Growing adoption of low/no-alcohol alternatives |

| Sometimes trying non-alcoholic options | 44% | 33% | Decline suggests users are shifting to more regular usage |

| Curious about non-alcoholic options | 20% | 24% | Continued expansion of the potential market |

| Would boycott misaligned brands | 53% | 54% | Stable overall, but intensity increasing |

| “Very likely” to boycott | 13% | 19% | Stronger conviction in values-based decisions |

| Home vs social drinking balance | More evenly split | Strongly home-dominant | Clear behavioral shift toward smaller, private settings |

Overall, Gen Z drinking behavior in 2026 shows a decisive shift toward moderation, home consumption, and more intentional, flexible alcohol use.

What happens if brands ignore these trends?

Brands that fail to adapt risk:

- Overestimating consumption frequency

- Missing the shift toward home-based occasions

- Underinvesting in non-alcoholic and flexible options

- Losing trust through lack of transparency

- Facing backlash from value misalignment

How can businesses use these trends to appeal to Gen Z?

Focus on occasion-based consumption: design products and messaging around when and how Gen Z drinks – not just what they drink.

Invest in low- and no-alcohol innovation: this is one of the clearest areas of growth and long-term relevance.

Prioritize convenience and format: ready-to-drink and easy-to-use formats align with real consumption behavior.

Build trust through reputation and consistency: brand perception and values increasingly determine who makes the shortlist.

Treat brand values as risk management: avoid misalignment – it carries more impact than positive positioning.

How Attest can help

Understanding how Gen Z consumers think, behave, and evolve over time is critical for staying competitive.

With Attest, you can:

- Track changes in consumer behavior year-on-year

- Compare segments and markets

- Test messaging and positioning

- Identify emerging trends early

All with fast, reliable insights from your exact target audience.

Research methodology

This multi-wave study explores alcohol consumption habits, preferences, and influencing factors among Gen Z consumers in the US. Data was collected across two waves: one in February 2025 and the most recent in February 2026.

Participants:

- 800 respondents based in the US, all English speaking

- Demographics:

- Ages 18-27

- Gender: 49% male, 51% female

- Regional quotas: Northeast (18.3%), Midwest (21.7%), South (37%), West (23%)